📊 Weekly Market Recap – 8/30/25

Fresh highs early, a risk-off fade into Labor Day

Hello traders and investors,

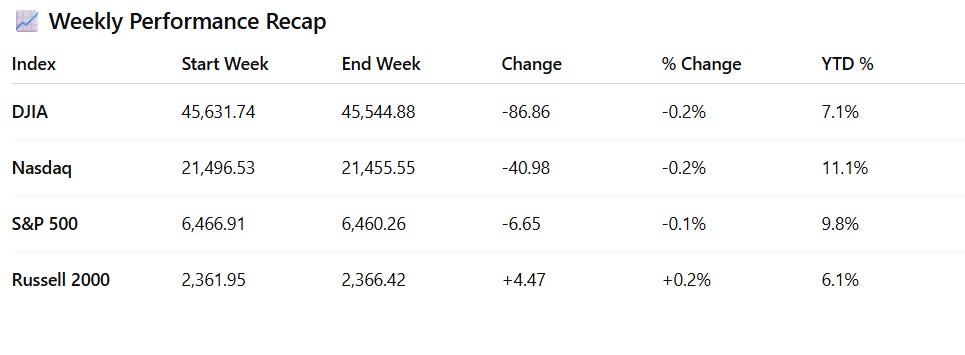

This week was a real tug-of-war. The market spent the first half chasing fresh highs and the back half bracing for risk. Monday opened soft with profit-taking after last Friday’s records, but momentum rebuilt from Tuesday through Thursday, carrying the S&P 500 to back-to-back record intraday and closing highs. Then Friday hit—a holiday-thinned session where sellers pressed on mega-caps, semis, and select cyclicals, leaving the tape looking tired into Labor Day.

🏆 Leadership & Rotation

Gains this week leaned heavily on mega-cap tech and communication names. On the green days, Alphabet, Meta, and Tesla did the heavy lifting, while the market-weighted S&P outpaced the equal-weight index, a classic sign that leadership narrowed.

Semiconductors were a mixed bag. NVIDIA’s earnings had the usual headline beats, but guidance wasn’t flashy, with export restrictions and zero China sales cooling sentiment. Marvell’s disappointing report on Friday pulled the whole group lower, leaving the SOX down 1.5% for the week, including a 3.2% hit on Friday alone.

Retail split in two: Kohl’s ripped on its EPS beat, but Best Buy, Dick’s, Dollar General, and Five Below turned in scattered post-earnings reactions.

Energy did its job quietly, supported by crude holding $64–65.

Defensives lagged early, but came back as the week wrapped in risk-off mode.

🏦 Macro & The Fed

Data came in balanced enough to keep rate-cut odds locked in.

Q2 GDP revised up to 3.3%, driven by net exports.

Durable goods and core capital goods showed firm demand.

Jobless claims stayed low, labor market still tight.

Weak spots? Housing (new & pending sales) and Chicago PMI, which cratered to 41.5.

The Fed’s preferred inflation gauge—PCE at 2.6% headline, 2.9% core—was sticky but right in line. That kept futures pricing a September 25 bp cut with 87–89% odds.

Fed officials lined up to keep things steady:

NY Fed’s Williams stuck with “data-dependent” and noted tariffs boosted PCE by 40–50 bps.

Richmond’s Barkin hinted at a “modest adjustment.”

Gov. Waller was more explicit, backing a September cut and expecting more in the next 3–6 months.

💵 Rates

Rates chopped around without much trend.

2-yr: 3.62%–3.73%

10-yr: 4.21%–4.28%

Long bond: 4.89%–4.91%

A midweek bull-steepener (short rates falling faster than long) gave way to a slight Friday retrace.

📰 Company Headlines

Keurig Dr Pepper dropped after a $15.7B cash buy of JDE Peet’s plus a split plan (North American beverages vs. stand-alone coffee).

Caterpillar fell Friday after citing tariff-driven margin pressure.

Dell & Marvell earnings disappointments weighed semis.

Alphabet & Meta helped comm services on up days.

Tesla extended early-week gains.

Trump vs. Fed Governor Lisa Cook: legal drama grabbed headlines but didn’t move the rate-cut needle.

🔑 Summary

This was a week of contrasts—early strength, record highs midweek, and a sour finish into Labor Day. The leadership is narrowing, semis cracked, and retail told a split story. Macro data was balanced enough to keep the Fed on track for September cuts, while company headlines added some volatility.

Markets are closed Monday for Labor Day. Expect volume to stay light early next week before traders return in full force.

Remember, I also post a free morning briefing before the open and a closing summary every day on Substack Notes and X — turn on notifications so you don’t miss them! EdwardCoronaUSA

*Disclaimer: The examples in The Options Oracle are my opinion, not financial advice.