🛞 Wheel Strategy Management Alert — $HUT Covered Call

💡Rolling the Wheel Forward: New Covered Call on HUT

I have a good entry today to start writing covered calls on HUT.

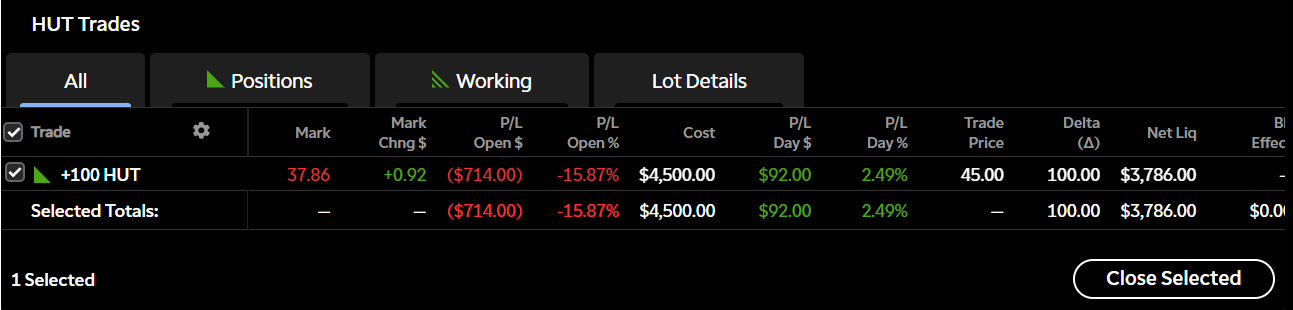

📌 HUT — Covered Call Update

Shares: 100

Current Price: trading in the high-$37s / low-$38s

CSP Assignment Cost: $45.00

Premium collected from CSP: $330

Effective Cost Basis:

$45.00 – $3.30 = $41.70

Today’s Price Action

HUT is green today, bouncing off the $35–36 area and pushing back into the upper-$30s. After several red sessions, this is the kind of relief move I look for:

Bounce off short-term support

IV still elevated

Better call pricing than earlier in the week

Momentum stabilizing after the selloff

That’s exactly when I want to sell calls.

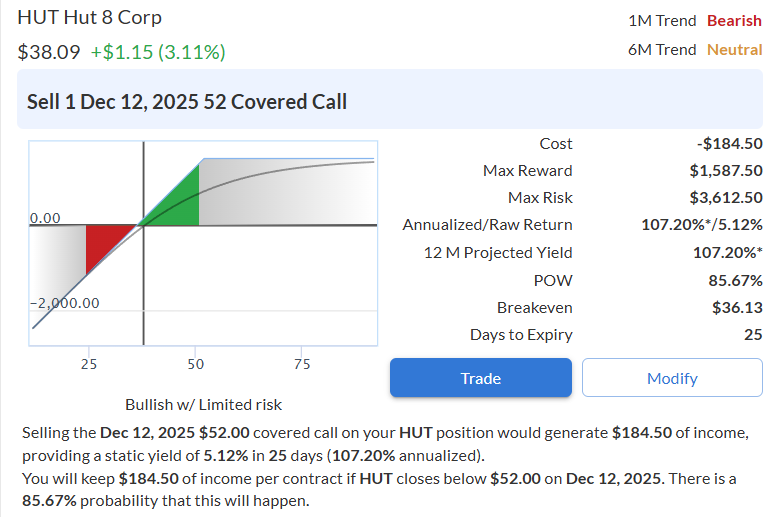

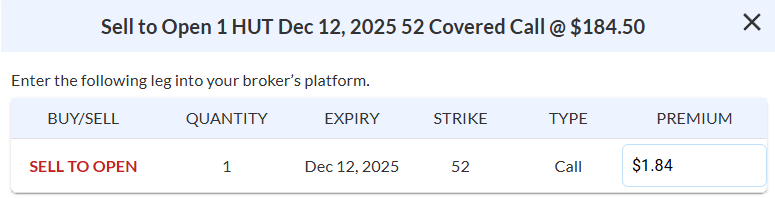

Today’s Play

This covered call alone lowers my basis from $41.70 → $39.86, and more importantly, it pays me to sit through the volatility instead of reacting emotionally.

Goal With Today’s Covered Call

Generate income while HUT stabilizes

Reduce cost basis even further

Let HUT rebuild trend without tying my hands

Set up a clean call-away only if HUT makes a decisive move higher

If HUT gets called away at $52, that locks in:

Profit from the CSP

Profit from the covered call

Stock appreciation from ~$39.86 → $52

That’s the full Wheel cycle working exactly as intended.

🧠 Strategy Notes

This trade is following the Wheel perfectly:

Sell CSP → Collect premium

Get assigned at a discount

Sell CC → Lower cost basis

Either keep stacking premium or get called away at a profit

The mission stays the same:

Generate continuous income

Keep lowering basis

Control risk during volatility

Let probabilities do the heavy lifting

Assignment wasn’t a problem — it was the next step.

*Disclaimer: The examples in The Options Oracle are my opinion, not financial advice.

11.17.25. Stock $38.57. Cost $41. Net debit (cost basis) after selling stock's covered calls $37.80.

Sold stock 11.21.25 (4 days) $41 strike (no gain) covered calls for $1.64 per share, or $164 per call option contract. Delta .41 (41% probability of being called). Implied volatility an extremely hit 158%. The bid asks on the call options are very wide. Options volume is low. I had to lower my ask price several times as the stock fell from its highs to get a fill. If the stock is called, the RoR will be 41-37.80=$3.20 per share, or 7.8%. The annalized RoR about 7.8 x 23=179.4%. Not bad. The 23 is the 23 trades that might be done if a trader did the same kind of covered calls trades about 23 times every 12 months. If I could do this covered call trade 23 times a year my per share premium income would be $1.64*23=$37.72 . It won't happen because prices fluctuate and I'm not perfect.:)